More and more asset owners pay attention to their Carbon Footprint, such as Fortune 500 companies. As we have mentioned already in our previous article “Carbon Footprint – Methodology”, the building sector is accountable for nearly 40% of annual global GHG (Greenhouse gas) emissions (9.2 GtCO2 in 2015 according to IEA).

This carbon footprint can be evaluated using the GHG protocol.

What is GHG protocol?

![]()

GHG Protocol is a guide helping how to quantify and report company, project or product GHG emissions. It has been developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD).

It covers six greenhouse gases identified in the Kyoto Protocol:

- carbon dioxide (CO2),

- methane (CH4),

- nitrous oxide (N2O),

- hydrofluorocarbons (HFCs),

- perfluorocarbons (PFCs),

- Sulfur hexafluoride (SF6)

All GHG emissions are converted into equivalent CO2 emissions: kgCO2e

Three different scopes are defined for GHG accounting and reporting purposes:

| Scope 1 | Direct GHG emissions from the company’s assets (fuel burning, use of company vehicles, processes inside company’s facilities…) |

| Scope 2 | Electricity Indirect GHG emissions for the generation of purchased electricity that is consumed in the company’s equipment or operations |

| Scope 3 | Other indirect GHG emissions (production of purchased materials and fuels, transport-related activities, product use by consumers…) |

Overview of scope definition in GHG protocol

Overview of scopes and emissions across a value chain as defined in GHG protocol

Global methodology

- Firstly, the organizational scope has to be set, so that emissions reflect the way in which the organization operates, not just its legal form. Either in ISO 14064-1 or GHG Protocol, it offers two choices of organizational perimeter:

- “equity share” reflects the financial participation of the organization in the issues of goods and activities; or by

- “control approach”, which includes the assets over which the company has control in financial or operation terms.

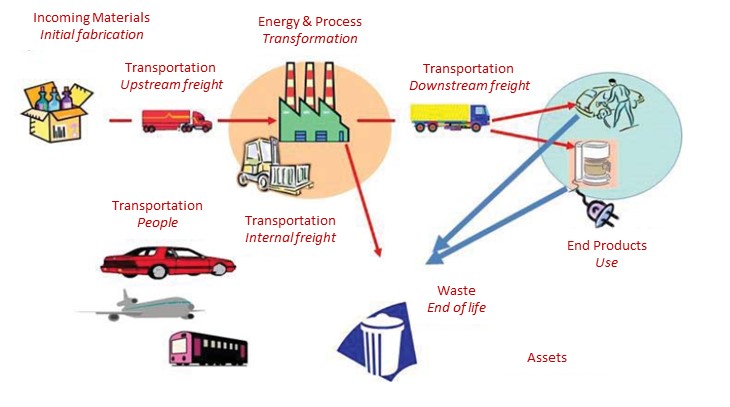

- Secondly, an operational boundary needs to be set, to determine which emissions are direct or indirect. Here the different Scope 1, 2 or 3 will be determined. It can be done by mapping energy and material flows, including the process below for instance:

- To start accounting for GHG, a base year needs to be chosen, for which the data will be compared. A base year should be the earliest with relevant data available.

- Identify and calculate GHG emissions: when the bases are set, we can start identifying sources from combustion, process emissions, fugitive emissions, etc. It would be done through a data collection campaign, where different department involvement would be needed (Facility, Operation, HR, Environment, Procurement…). Then the next step is to calculate the GHG emissions, as the direct measurement of GHG emissions is not common. Emission factors would be chosen for each type of fuel, process, etc. through documented emission factors, such as IPCC guidelines (IPCC, 1996).

- After the calculation is carried out, the last step is to report the data to the corporate level.

- It will enable the establishment of an action plan to reduce the carbon footprint. It may influence the company’s energy policy, reflect on logistics circuits, and suggest awareness-raising actions, etc.

GHG Protocol or ISO 14064-1?

ISO 14064-1:2018 – Greenhouse gases – Part 1: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals) was first published in 2006, and is based on GHG Protocol. Scopes are not defined in the ISO standard, but they follow the same principle of organizational and operational boundaries, Direct and Indirect emissions (without scopes). It is a minimum standard to follow, rather than a detailed guidance.

The ultimate goal of both standards is in the end the same and they will help to cover the assessment of similar greenhouse gas emissions.

If you need a carbon footprint assessment of your asset, you can contact our BD manager Gaspard at glemsce@teraochina.cn. We would be glad to accompany you to assess your assets carbon footprint, in order to make the right decisions on how to reduce it and implement an action plan.

Leave A Comment